It might not be a secret to anyone that Russia’s coal industry has been pivoting towards Asia – domestic utilization of the country’s vast coal reserves is stagnant at best, however its exports towards China, Japan and other Asia Pacific consumers have been increasing at a constant rate, recurring crises notwithstanding. Yet up until now Russia’s coal industry was functioning in a conventional way, whereby both production and exports were carried out by coal-focused companies, with little to no interference from firms from other segments. Now one of the most peculiar developments in Russia’s coal was the recent takeover of the Elginskoye mine with 2.2 billion tons in total reserves, sold by Mechel to A-Property, a company headed by Albert Avdolyan with no previous exposure to large-scale energy projects and a heavy background in telecommunications/IT. Mechel is one of the ultimate survivors of Russia’s energy scene. Having accumulated a whole array of assets in the country’s Far East in the Golden Era of the 2000s, the financial crisis of 2008/2009 has crippled its finances and launched a decade-long history of debt restructuration. Mechel’s market capitalization was further weakened by then-Prime Minister Putin’s repeated rebukes against the firm’s alleged practices of overpricing coal supplies to the domestic market. Between 2008 and 2012 Mechel’s debts doubled from $5 billion to $9.6 billion, further aggravated by unnecessary acquisitions and the post-2014 economic stagnation of Russia. Luckily for Mechel, its main lenders were state-owned banks that turned out to be rather cooperative vis-à-vis the company, agreeing to a 5.1 billion restructuring deal in 2017. Yet the coal depression of 2019/2020 brought Mechel’s odyssey with the Elginskoye mine to an end.

The new owners of Elginskoye intend to invest $2 billion into the coal mine, bringing total production from its current level of roughly 5 million tons per year to 45 mtpa, which would make it the third-largest mine globally in terms of annual output. To this end A-Property wants to build a new mining and processing plant with a 1st phase nominal capacity of 32mtpa (by 2021) which would be increased with the project’s 2nd phase to 45mtpa by 2023. Even at the heyday of Mechel’s ambitious plans, the company planned annual production to plateau at some 30 mtpa, so the new owner’s plans have surpassed all previous expectations. Ramping up production and processing in itself would not be enough – the produced coal needs to find its way towards the Asia Pacific market and needs dedicated rail conduits to get the crude from landlocked Yakutia to the Pacific coast.

When it comes to infrastructure, A-Property has been lucky again with Mechel blazing the trail – the Elginskoye coal mine is connected to the Baikal-Amur Mainline (one of Russia’s largest transportation conduits that runs parallel to the Trans-Siberian railway) via the Elga-Ulak feeder line, 321-kilometer long. The new owners are claiming that they would try to increase the feeder throughput capacity almost fourfold to 12mtpa by the end of this year, to 24mtpa by the end of 2021 and to 30mtpa by 2023. Enhancing the feeder line, in effect built specifically for the Elginskoye mine and heretofore the only railway line to be built by a private entity, might still be feasible if the new owners can maintain the level of financing they’ve pledged. Finding a suitable port might turn out to be a bigger problem.

Regional authorities have already welcomed the Elginskoye developments, having lamented recently that Mechel massively underperformed its objectives – instead of the 20mtpa set for 2020, the coal mine would still only be a quarter of the target, depriving the Yakutia budget of much-needed revenues.

Federal authorities have been tacit so far yet they, too, have every reason to support the current outcome – Russia’s ambitious coal export plans (the „ambitious” scenario stipulates an output hike of 51% by 2035, to 668mtpa; the conservative scenario foresees an increase of 10% to 485mtpa) have been hindered lately by Mechel’s survival struggles. Federal banks seem to be also satisfied that the ever-looming threat of Mechel going bust is now alleviated by the sale of Elginskoye.

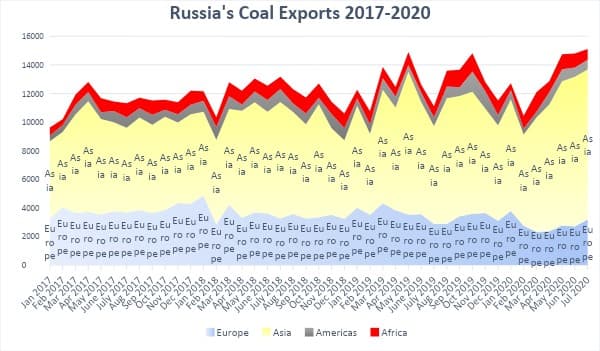

Graph 1. Russia’s Monthly Seaborne Coal Exports by Continent in 2017-2020 (thousand tons).

All in all, Russia’s coal exports have seen a spectacular surge after the 2008 crisis watershed – after it, internal consumption has started to gradually decrease all the while production kept on rising. The overall output volumes could have grown even further, were it not for the 2019 coal price drop which has tempered the appetites of Russian producers. General coal-related skepticism and this year’s COVID-depression will halt Russian coal exports for a while, in the meantime though Russia has been working on clearing all the logistics constraints that have hindered Asia-bound supplies previously. As exports to Europe seem to be evaporating completely, preparing all the Asian rail infrastructure before producers actually see the coal demand they are expecting makes commercial sense.

It is difficult to assess A-Property’s long-term goals with one of Russia’s largest coal mines and certainly the hottest prospect on its roster. As opposed to the oil and gas sector, both of which experienced a palpable period of ownership rights’ regression after the fairly liberal period of the 1990s, Russia’s coal sector does not have a state-owned national champion, hence the usual suspicion of the government preparing itself for a sudden nationalization does not seem to be the most likely scenario (though certainly not impossible, with A-Property then acting as a temporary asset developer). If A-Property is indeed interested in committing to coal in general and the Elginskoye mine in particular, it might provide the first pioneering case for Russia when IT capital (probably the only one today that is reasonably immune to government intervention) has kickstarted a major hydrocarbon cluster.