Albemarle’s decision to place its Kemerton lithium hydroxide processing plant in Western Australia into care and maintenance has underscored the structural challenges facing Australia’s downstream lithium ambitions – but it may also mark a pivotal reset for domestic players seeking to scale value-added processing.

The US-based lithium producer confirmed it would idle operations at Kemerton immediately, following earlier moves to cancel expansion works (Trains 3 and 4) and mothball the site’s second production train. More than 250 jobs are expected to be lost, with dozens of contractors also affected.

Albemarle chairman and chief executive officer Kent Masters described the move as a difficult but necessary step amid prolonged lithium price volatility.

“Idling operations at Kemerton was a difficult decision. It follows significant actions we have taken over the past two and a half years to reduce operating costs during an extended period of price volatility in the market,” Masters said.

“Unfortunately, recent lithium price improvements alone are not enough to offset the challenges facing Western hard-rock lithium conversion operations. This decision improves our financial flexibility and preserves optionality.”

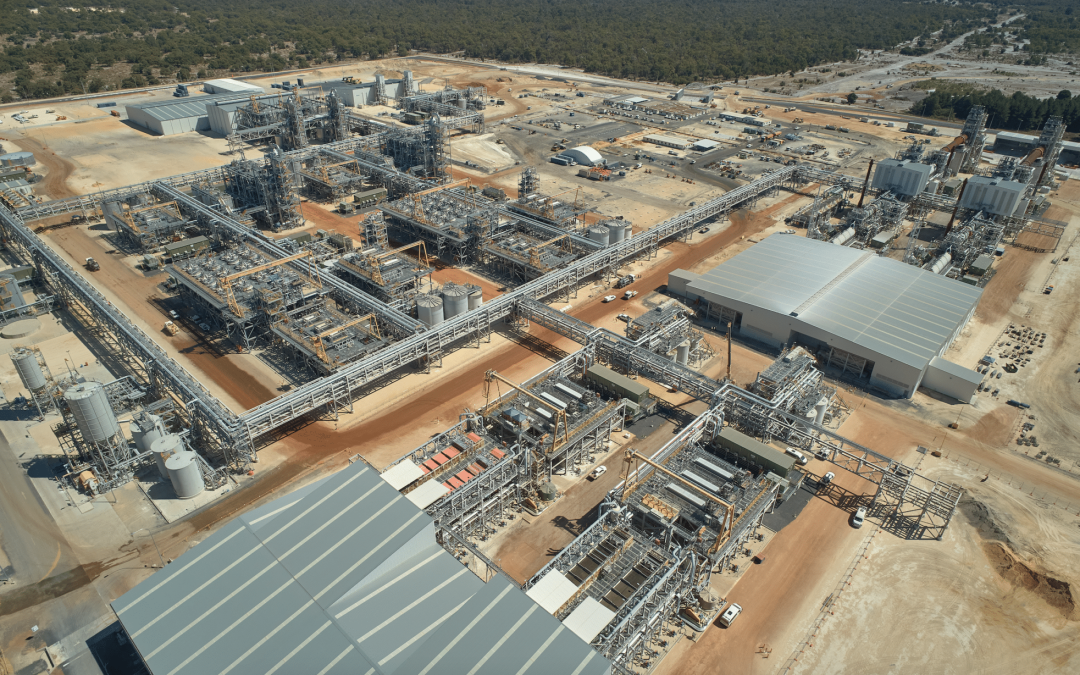

The Kemerton plant processes spodumene from the Greenbushes mine, one of the world’s best spodumene resources. Albemarle holds ownership interest and half of the offtake rights from Greenbushes through an Australian joint venture.

Yet while the closure is a setback for Western Australia’s processing narrative, it leaves behind strategically valuable assets: established infrastructure, skilled labour, regulatory approvals and proximity to world-class hard-rock lithium deposits.

Kemerton is not the only refinery to have faced pressure. The Tianqi Lithium Energy Australia (TLEA) refinery in Kwinana – a 51 per cent Tianqi Lithium and 49 per cent IGO joint venture – was the first lithium hydroxide plant built in the industrial precinct. Designed for 24,000 tonnes per annum of lithium hydroxide production, the facility has struggled to achieve consistent profitability amid weaker lithium prices and operational challenges. As of August 2025, IGO reported low confidence in the asset, citing losses and the need to materially improve efficiency.

Taken together, the experience at Kemerton and Kwinana highlights a clear lesson: downstream lithium processing in Australia requires scale, integration and disciplined cost control to compete in a market long dominated by Chinese converters.

For well-capitalised Australian groups, however, the opportunity remains compelling.

Association of Mining and Exploration Companies chief executive Warren Pearce told the Australian Financial Review the closure of Kemerton might not be permanent.

“Although today’s decision is set back, it is hoped that when market conditions improve, this world-class asset will be able to return to operation,” he said.

Companies such as Wesfarmers have already signalled long-term ambitions in battery materials. Through Covalent Lithium – its 50-50 joint venture with Chilean company SQM – the company operates the Mount Holland mine and concentrator and the Kwinana refinery, which is ramping up towards approximately 50,000 tonnes per annum of battery-grade lithium hydroxide.

Wesfarmers chief executive Rob Scott has previously highlighted lithium hydroxide as central to Australia’s export diversification strategy, alongside the company’s broader chemicals, energy and fertiliser portfolio under WesCEF.

Kemerton’s idling also coincides with new federal policy settings aimed at strengthening domestic processing. From mid-2027, eligible lithium hydroxide producers will qualify for the 10 per cent Critical Minerals Production Tax Incentive, improving long-term project economics. Combined with the Federal Government’s push to build resilient, non-Chinese critical minerals supply chains, the policy environment is becoming increasingly supportive of downstream investment.

Resources Minister Madeleine King, who met with Albemarle executives during last week’s Critical Minerals Ministerial in Washington, acknowledged the disappointment of the decision but reinforced the broader strategic imperative.

“It can be an immense challenge for projects to compete in global supply chains that are concentrated, opaque and subject to market distortion,” King told the Australian Financial Review.

For Australia’s mining sector, the challenge now is not whether lithium processing can be done domestically, but how it can be structured to succeed. Greater vertical integration between miners and refiners, disciplined capital deployment, long-term offtake partnerships and policy certainty will all be critical.

Hard-rock lithium remains one of Australia’s strongest competitive advantages. With electrification demand expected to underpin long-term consumption growth, the recent refinery setbacks may prove less a retreat and more a recalibration – opening the door for a more resilient, Australian-led processing model built on lessons learned.