In June, the White House released the findings from a hundred-day review of supply chains that are critical for US interests. The roughly 250-page report comprises several studies from the US Departments of Energy, Commerce, Defense, and Health and Human Services, and it outlines a number of important recommendations for improving supply chain resiliency.

A particular area of focus within these recommendations is the need to ensure the availability of key minerals and materials, especially those critical to the deployment of advanced batteries and other renewable energy technologies, namely lithium, cobalt, nickel, copper, and rare-earth elements (REEs).

These recommendations include increasing US activity throughout the minerals supply chain by stimulating downstream demand, supporting innovation (especially in mineral recycling), calling for more domestic mining and processing activity for key minerals, and coordinating closely with allies and partners around the world.

All graphics taken from “Building resilient supply chains, revitalizing American manufacturing, and fostering broad-based growth” – 100-Day Reviews under Executive Order 14017, June 2021. A report by The White House

Although the recent hundred-day review is an important step forward as the United States begins to address the challenge of mineral supply chains in the energy transition, the report highlights several key themes that policymakers will continue to grapple with as they begin to implement its recommendations.

1. The role of the U.S. within rapidly growing mineral demand

Following the release of the International Energy Agency’s report on The Role of Critical Minerals in Clean Energy Transitions this April, which forecasts a four-fold increase in demand for key minerals in order to meet the goals of the Paris Agreement, the White House’s review further brings into focus the role of the United States in that global demand growth.

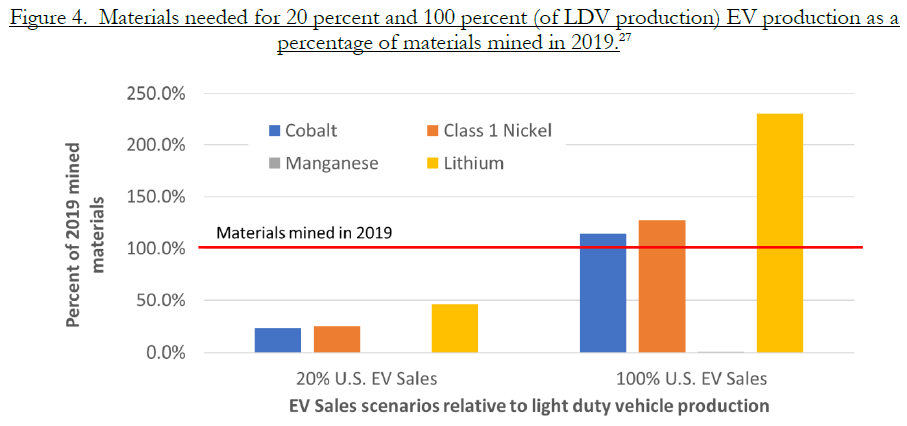

For example, the report projects that the minerals required to electrify 20 percent of the US light-duty vehicle fleet with lithium-ion batteries will constitute approximately 25, 49, and 22 percent of the total nickel, lithium and cobalt (respectively) that was mined in 2019. Those same mineral requirements grow to an estimated 127, 245, and 114 percent of 2019 production to electrify 100 percent of the fleet.

Replicate that across a number of renewable energy and decarbonisation technologies as the Biden-Harris administration deploys an ambitious plan for a domestic energy transition, and the United States is poised to become one of the largest centres of global demand for critical minerals.

2. Clarifying “risk” in the minerals supply chain

Second, the review makes a point to highlight the risks of a passive US approach to growing mineral demand, noting the effects of several supply chain disruptions over the past decade. However, policymakers would be wise to frame these risks appropriately. For many renewable energy technologies, mineral supply chain risks are different to traditional energy security concerns.

Unlike an oil price crisis or gas embargo, mineral supply disruption will have less of an impact on the ability of an electric vehicle to take someone from point A to B or for a solar panel to generate electricity, but will rather impact the pricing environment to deploy those technologies in the first place.

The risks of the mineral supply chain, therefore, are more closely associated with long-term challenges such as economic security, decarbonisation goals, and technological leadership, underscoring the importance of a holistic strategy rather than just patching supply chain vulnerabilities.

3. Focusing in on individual mineral criticality

Of the thirty-five minerals and sub-metals that are deemed critical by the United States, the review makes important distinctions between the nuanced supply chain characteristics of each individual mineral for which the United States is import dependent. To this end, there are several valuable instances throughout the report where specific minerals and mineral risks are evaluated relative to each other.

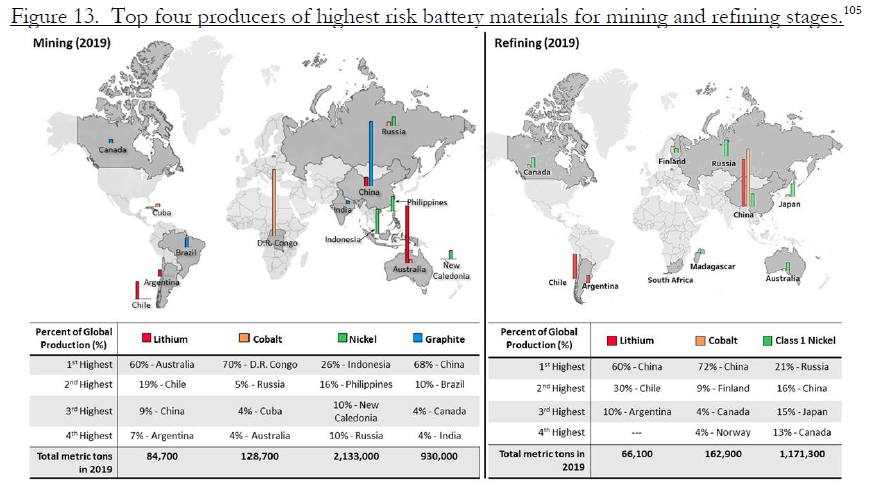

For example, in one instance the report de-emphasises “graphite and manganese as materials of greatest concern (in relation to Class 1 nickel) compared to other more generalised US government assessments.” Further on, there is also an assessment of relative mineral import reliance in comparison to global production.

Given the diverse set of minerals the United States has deemed critical and the expected acceleration of supply chain concerns as global demand picks up in the next decade, US policymakers will need to build upon these types of analyses to re-evaluate each mineral’s relative criticality to implement policy and deploy financial capital where it can be most effective in a short amount of time.

4. Domestic mining and permitting

At the core of the review’s recommendations is the ambition for increased US production and processing of key minerals to help meet domestic demand. However, it reveals a key tension between the need to facilitate a permitting structure that ensures best-in-class standards for sustainability, land use, and local stewardship, but which effectively meets the urgency of expected demand growth in a short time period.

This tension is given limited attention. Certain sections call for additional precautions within the permitting process, while others note the near ten-year timeline for a new mining project independent of permitting activities, and highlight the need to identify efficiencies to access domestic resources more quickly.

The White House’s fact sheet, meanwhile, calls for an interagency review of gaps in statutes and regulations that will need to be addressed to uphold high sustainability standards. However, the fact sheet also highlights a need to “identify opportunities to reduce time, cost, and risk of permitting without compromising strong environmental and consultation benchmarks.”

This suggests that movement on either side of the permitting challenge is still very much on the ‘to-do’ list even as it becomes a central policy debate around the desire for increased domestic mining. As the administration begins its implementation of the recommendations within the review, how it navigates this balance will be a key area to watch.

5. The importance of allies and partners

Finally, the report makes clear the need for continued engagement with allies and partners such as the European Union, Canada, Australia, and Japan in improving mineral resiliency. Notably, that engagement is contextualised in the review as part of a broader vision for US engagement in the upstream minerals supply chain, which follows reporting last month that the United States might rely on international partnerships for the majority of its mineral needs at the expense of domestic mining and processing.

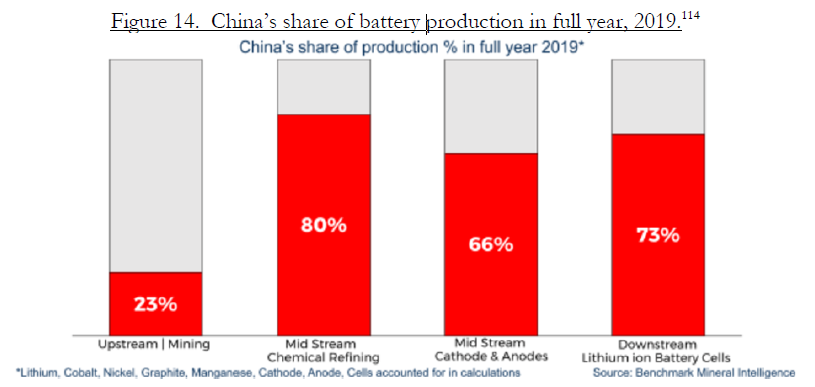

This contextualisation is important for two reasons: first, meeting the scale of expected mineral demand requires an expansion of US engagement in both the international and domestic pieces of the mineral “upstream,” and second, building international partnerships as part of a holistic approach to mineral resiliency is absolutely necessary to reduce supply-side risks, particularly risks associated with China’s dominant role in key segments of the global mineral supply chain that are highlighted throughout the review.

All told, this hundred-day review provides the fullest picture thus far of how the administration is evaluating the issues of mineral access and supply chain resiliency. Yet the review is still a first step (albeit an important one). Given President Biden’s well-articulated goals for US re-engagement in the energy transition at home and abroad, the challenges and opportunities of increased demands on mineral supply chains will only grow. Therefore, how the administration approaches the implementation of the recommendations within this review—particularly in relation to the themes discussed above—will provide critical insight into its broader strategy to ensure robust, secure, and resilient mineral supplies.