The upward trend in the carbon price since 2015 has already seen coal generation decline significantly. Last year, total generation was a little over 100 TWh; it was 263 TWh in 2003. Sebastian Ligewie at Energy Brainpool looks at the prices of hard coal, lignite and the EUAs (EU emission allowances). It’s around €37 per MWh for hard coal and €8 for lignite. But emissions costs of around €63 per MWh for hard coal and €84 for lignite are added to that (assuming a certificate price of €85). If the certificate price permanently rises above the €100 threshold, things will become very tight for coal, says Ligewie. And with declining energy consumption in Germany, cooling gas prices and a flood of cheap renewable energy, coal could disappear by 2030 whether there is a new phase-out law or not.

Coal will be phased out of the German electricity mix by the end of 2038 at the latest. The last coalition led by Chancellor Angela Merkel had already agreed on this. If the current coalition government has its way, the coal phase-out would ideally be completed by 2030.

What role does coal, once the most important energy source in the German electricity mix, still play today?

Coal’s recent history

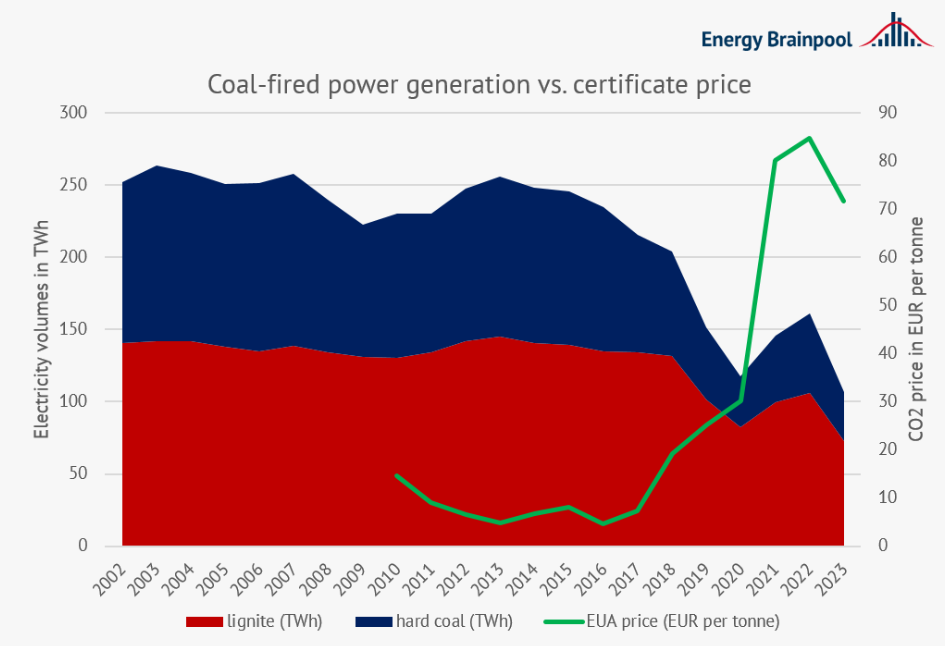

If we look at the amount of electricity generated from lignite and hard coal since 2002, we can see a clear trend, at least in the recent past: coal is running out of steam! In 2003, around 263.6 TWh were produced from lignite and hard coal. As of December 7th 2023, only 106.7 TWh have been produced. Of course, that doesn’t include the last few weeks of the year.

Nevertheless, we can already say that it will only be a fraction of the former coal volumes. The rapid downward trend began in 2015, with only the gas crisis years of 2021 and 2022 giving coal a brief renaissance. Now the gas markets have calmed down again significantly. This has set coal back again. It is interesting to note that the decline in coal-fired power generation almost exclusively affected hard coal. Lignite, on the other hand, lost much less of its share. But how can we explain these trends?

EU emission allowances (EUAs)

As always on the energy market, there are a number of factors at work here. Basically, these include declining energy consumption, cooling gas prices and a flood of cheap renewable energy. However, there is another decisive factor that is putting coal under increasing pressure: EU emission allowances (EUAs). In the period from 2010 to 2017, the certificate price was below 10 euros per tonne of CO2. In the years that followed, the upward trend intensified further and then stabilised at around EUR 100 at the end of February 2023. The price has since cooled down again somewhat. It remains at a significantly higher level. But what effects do these prices have in practice?

Figure 1: Combined lignite and hard coal power generation & average certificate price based on EntsoE and EPEX Spot data / SOURCE: Energy Brainpool

CO2 price in practice

If you want to allocate the certificate prices to the production costs of the various fossil fuels, you can do this in a simple calculation example. To estimate the emissions intensity – and thus also the certificate costs – we take the figures published by the Federal Environment Agency on primary energy sources(1) and the average efficiency of the German power plant fleet(2). Together with the current fuel prices, we can then roughly estimate how much a megawatt hour costs to produce.

Unsurprisingly, coal is hit much harder by certificate prices than lower-emission gas due to its higher emissions intensity and the comparatively low efficiency of the power plants. Coal still benefits from comparatively low fuel costs. They are around 37 EUR per MWh for hard coal and 8 EUR per MWh for lignite. Despite this, emissions costs of around EUR 63 per MWh for hard coal and EUR 84 per MWh for lignite are added to this, assuming a certificate price of EUR 85.

Lignite has declined less than Hard Coal

Under these assumptions, the entire electricity generation from lignite is even cheaper than from hard coal due to the cheap fuel. Even if the latter is more affected by the price development of certificates due to its higher emissions intensity. This competitive advantage explains why lignite-based electricity generation has been less affected by the decline in recent years than hard coal.

Gas and steam power plants are among the options available for generating electricity from gas. These have the advantage that they are significantly more efficient than coal-fired power plants and use a fuel with lower emissions. This makes them direct competitors to coal in the merit order. The costs here amount to 25 euros per MWh for emissions and 70 euros per MWh for the fuel.

Although natural gas is more expensive as a fuel, these additional costs are almost completely offset by lower emission costs in this calculation example. As we are using average values here, individual power plants that are new or particularly efficient may have higher efficiencies. In individual cases, this can already lead to CCGT power plants outperforming some coal-fired power plants in the merit order.

Do we need to phase out coal?

The numbers game should make one thing clear: in future, the certificate price is likely to increasingly determine whether coal-fired power plants run or not. If the certificate price permanently rises above the 100 euro threshold, things will become very tight for coal under absolutely identical circumstances. At the same time, we also need a significant acceleration in the expansion of renewables.

If rising certificate prices and the expansion of renewables come together, what the then CEO of RWE, Martin Schmitz, predicted two and a half years ago could come true: “(…) that the coal phase-out in 2030 is practically “done” – even without a new law.”